Palantir just delivered one of those updates that looks strong at first glance, but gets more nuanced the deeper you go. The company beat expectations, raised its full-year outlook, and continues to ride the AI wave. But there are also clear signals investors should not ignore.

Let’s break it down.

What worked

-

Revenue beat

Q1 revenue came in at $1.63 billion, ahead of the $1.54 billion expected. That is a solid beat and shows demand is still holding up. -

Full-year outlook raised

Palantir now expects $7.65 billion to $7.66 billion in annual revenue, significantly higher than its earlier guidance of around $7.19 billion. This is the biggest positive from the update. -

Government business remains strong

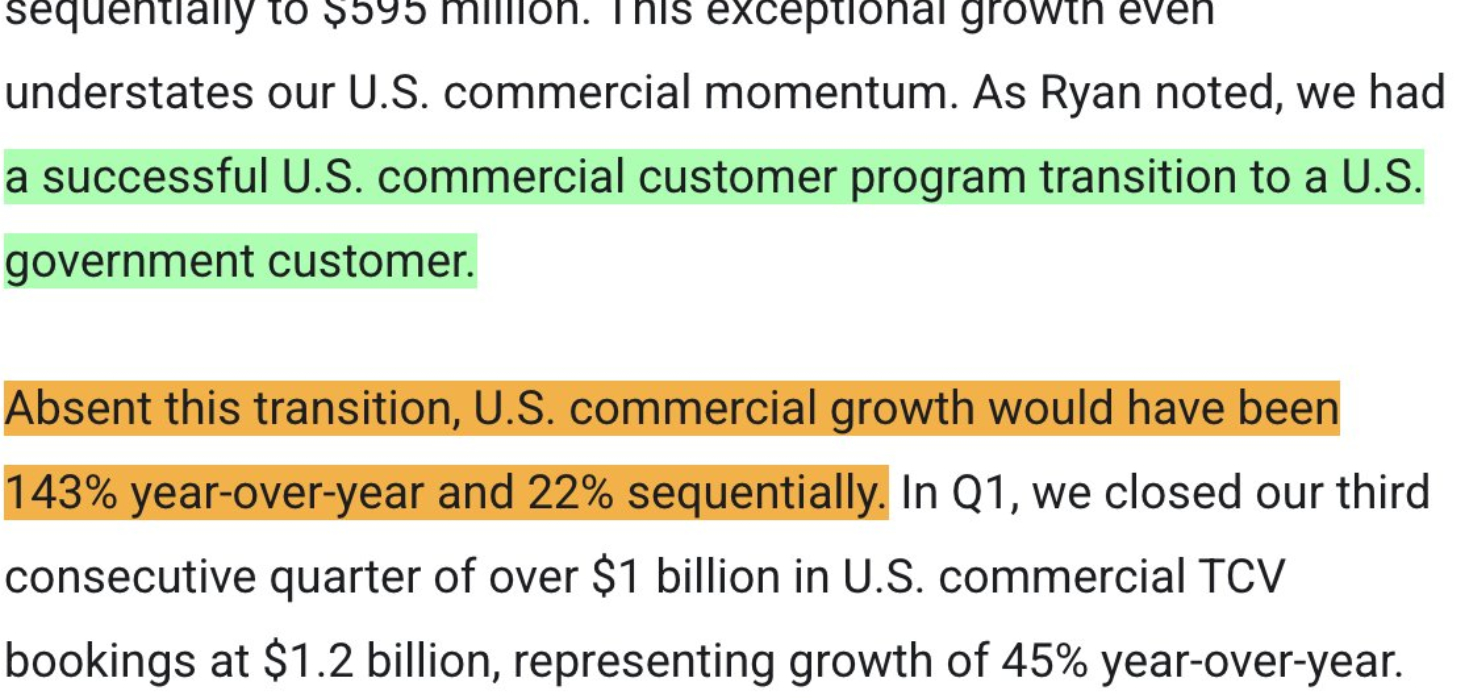

US commercial sales looked weaker than expected

Reported US commercial revenue came in at $595 million, below expectations. However, management clarified that a large customer transitioned from the commercial segment to the government segment during the quarter, impacting the reported figure. -

AI positioning still intact

The company remains one of the earliest public market beneficiaries of the AI boom, especially in defense, intelligence, and enterprise data.

What didn’t work

-

US commercial sales disappointed

This is the biggest weak spot.

Revenue came in at $595 million, missing market expectations. -

Overdependence risk showing up again

Government contracts are still driving growth. That is stable, but it also limits how scalable the story can be compared to pure enterprise software peers. -

Competition is rising

As AI tools become more accessible, more companies can build similar capabilities. The moat is not as untouchable as it once seemed.

The bigger picture

Palantir sits in a very unique position.

- It is deeply embedded in government and defense ecosystems

- It is pushing aggressively into AI-driven software platforms

- It has a strong narrative around national security and AI

At the same time:

- Its commercial adoption is still inconsistent

- Its brand and positioning remain polarizing

- Its growth quality is still debated

This is not a clean SaaS story. It is a mix of defense tech, AI infrastructure, and enterprise analytics.

Market reaction and sentiment

- The stock is still down about 18 percent this year

- It saw a small bounce of around 1.3 percent in after-hours trading

This tells you something important.

The market likes the numbers, but is not fully convinced.

What to watch next

- Can commercial revenue catch up with government growth

- Whether AI-led demand translates into repeatable enterprise adoption

- How competition impacts pricing and margins

- Continued government deal flow, especially from the US

Bottom line

Palantir is still executing, and the raised guidance proves demand is real.

But this is not a straightforward growth story.

It is a company benefiting from powerful trends, while also dealing with structural questions around scalability and competition.

For investors, the key question remains simple:

Is Palantir an AI platform that can scale globally, or a high-quality niche player tied closely to government spending?