1/ $HOOD now has three revenue channels driving growth:

- Trading revenues.

- Net interest revenue.

- Other product revenues.

All these segments are growing really fast.

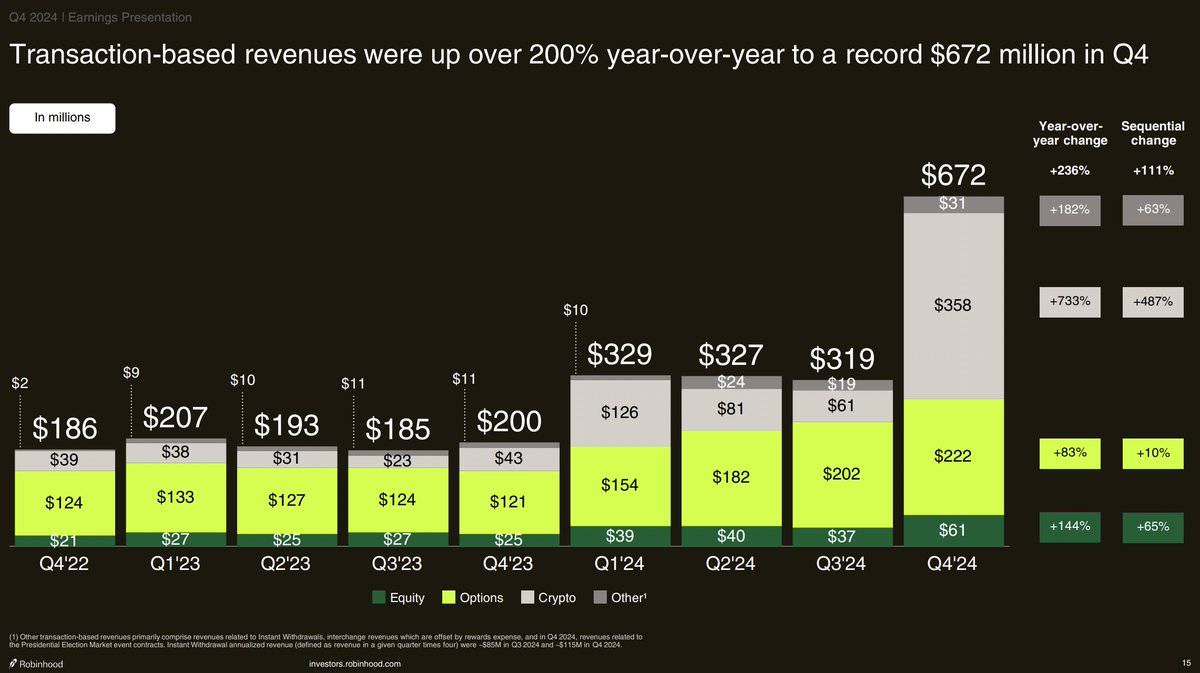

Here is how they performed last quarter ![]()

2/ Trading revenues are exploding.

This segment grew 200% year-over-year while net interest revenue increased 25% and other product revenues grew 31%.

Though this growth looks appealing, it’s just the beginning…

Let me explain why:

3/ It’s simply crypto.

Most of the growth in transaction revenues was driven by crypto.

While transaction revenues from equity doubled, crypto revenues grew nearly 10x since Q4 2023.

There are two drivers here: Crypto prices and international expansion.

Here is how it works:

4/ RobinHood generates transaction revenues through:

- Order flow arrangements.

- Markups on the crypto prices.

Both of these work on a percentage base on the crypto price, meaning RobinHood’s cut increases as the crypto prices increase.

This isn’t going to slow anytime soon.

As big asset managers like BlackRock constantly grow their $BTC holding, the price will keep surging.

And so will RobinHood’s transaction revenue.

5/ It’s also growing internationally, rapidly expanding transaction volume.

RobinHood crypto launched in EU in Q1 2024 and expanded capabilities throughout the year. This doubled the TAM instantly.

Yet, it still doesn’t offer crypto trading any other region.

As it enters new markets, trading revenues will explode.

6/ Its interest revenues will also explode as assets under custody (AUC) grows.

It grew AUC 88% last quarter to the record high of $193 billion.

This may look a lot but’s actually still small given Schwab has $4.2 trillion under custody.

RobinHood AUC will grow fast as the current users increase their net worth and it attracts more users through offers like 1% match.

This segment can easily grow 10x in the next 5 years.

7/ Growth will reaccelerate as gold adoption increases.

Average gold member has 5x more assets under custody and 1.5x faster deposit growth than a normal user.

It also charges $5 monthly fee to gold users.

Subscription fees alone generate $128 million a year currently. This may look small but it’s 100% gross margin.

As gold adoption increases, both interest from AUC and trading revenue will grow even faster.

8/ Annual revenue per user (ARPU) will expand significantly.

RobinHood’s ARPU currently stands at $164 level, while legacy investment houses like Schwab have ARPU between $500-$700.

As RobinHood users increase their net worth and time spent on the platform, ARPU will converge to that of the traditional investment houses.

This will also drive significant revenue growth.

9/ It’s financial position is also rock-solid.

It has $7.9 billion equity against $7.3 billion debt. It also holds $5 billion cash on the balance sheet.

This provides it with a significant legroom to ramp up investments for growth.

10/ Valuation is still attractive despite the recent surge.

Last year, it grew revenues by 58% and generated $3 billion revenue.

Even if we assume that growth declines to 30% annually in the next 5 years, it’ll generate $11 billion revenue by 2030.

Other investment houses like Schwab has 30% net profit margin.

Given that $HOOD is fully digital and don’t have much of the traditional expenses, it can easily pull up this number to 35%.

This gives us $4 billion net income for FY 2030.

Attach it a conservative 30 P/E and we have a $120 billion business.

It’s currently valued at only $55 billion.

From X

Good article

Good article Not helpful

Not helpful